By Patrick Sullivan, Film & TV Editor

Many students bemoan of ‘extortionate’ tuition fees, but the loan system is designed to eradicate any harsh, financial implications of going to university to such an extent that it is uncertain whether a student will pay anything. The real financial burden when studying is the varying living costs of the cities students live in.

The student loan system in the UK has been featured in national news regularly since the controversial inception of £9000 annual fees for undergraduates in 2010. From September 2012, most British undergraduate students have paid - or, more accurately, borrowed - £9000 per year of study, with no stipulations of subject. The relatively high fees and graduate ‘debt’ have been a common conversation for students and taxpayers alike in the years since.

The money for both tuition fees and maintenance loans are provided by the Student Loan Company (SLC), a ‘non-profit making, Government-owned organisation’. However, HMRC, responsible for collecting all taxes, assist the SLC with servicing and ensuring repayments of those loans. When analysing the loan system, there is little differentiation between the repayment of student loans and the concept of ‘graduate tax’, except for student ‘debt’.

Key facts about student loans:

- You only repay 9% of your earnings above £25,000.

- An interest rate of 6.3% (3% + RPI) is added even while you study.

- 75% of future graduates are predicted not to fully pay off their student loans.

- All remaining student loan repayments are written off after 30 years.

- The average UK salary is £29,588, including non-graduates (ONS). **

University tuition fees could be cut to £6,500 under proposals from a commission established by Theresa May to recommend higher education reforms https://t.co/a9TtVIYl18

— The Times of London (@thetimes) November 3, 2018

The strict definition of debt is ‘the state of owing money’. The way student loan repayments are structured however is by paying nine per cent of all earnings above a certain threshold. Until April 2018, that threshold was £21,000. Now, however, it is £25,000. Associated with debt is the pressure to pay back any money owed and the effect of interest if you are slow to pay it off. While interest rates have become a larger factor over time - they have risen from 3.9 per cent to 6.3 per cent since the 2015/16 academic year and are applied even during years of study - there is no pressure to ever pay off your student loan. Therefore, it is difficult to class as debt, especially in the same sense as payday loans or harsher, long term loans like mortgages.

A report published in July 2017 by the Institute of Fiscal Studies (IFS) was conclusive in the uncertainty caused to both students and the government by the repayment structure. The amount repaid to the government is entirely dependent on future graduate earnings, a value made even more difficult to predict when considering the rise in student population - nearly 28 per cent of English 18 year olds started University in 2018, 96 per cent of whom took a student loan. How can the government predict the earnings of such a large group of varied students?

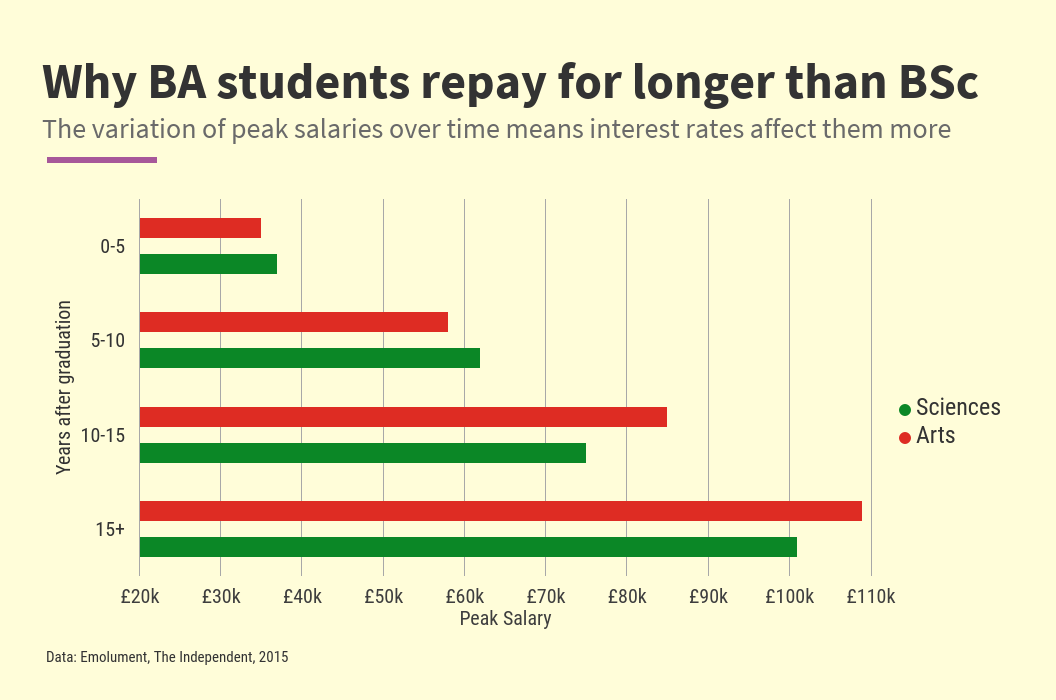

On November 2, it was reported that the governmental review of higher education, due to be published in the new year, will recommend decreasing fees to £6,500 for Arts degrees and increasing them to £13,500 for higher earning degrees such as Medicine or Engineering. The financial illusion of having to pay that money could discourage lower income students from doing subjects like Medicine and, likewise, discourage universities from offering so many places for Arts and Humanities.

However, from early analysis in The Times, it would not hugely affect the amount students repay but simply keep higher earning BSc graduates repaying the same rate for longer. Arts students are more likely to form part of the 75 per cent of graduates the IFS predicts will never fully pay off their student loan, but that is because their degree is not tailored to specific employment channels rather than lower prospects. Arts students take longer to reach their peak salaries, by which point interest has kicked in. Lower tuition fees would allow them to repay their debts faster, but when they earn more later, they would be avoiding any further repayment.

(Epigram / Patrick Sullivan)

The government writes off any outstanding ‘debt’ 30 years after graduation, and this report proves their desire to keep the high earners contributing for as much of that period as possible. It begs the question: why not simply charge an extra graduate tax of nine per cent for all earnings above £25,000 for 30 years post graduation, regardless of subject? It would certainly improve the attitude of a student population who constantly berate having to ‘pay’ £9,000 a year when, in fact, they may never have to pay anything at all.

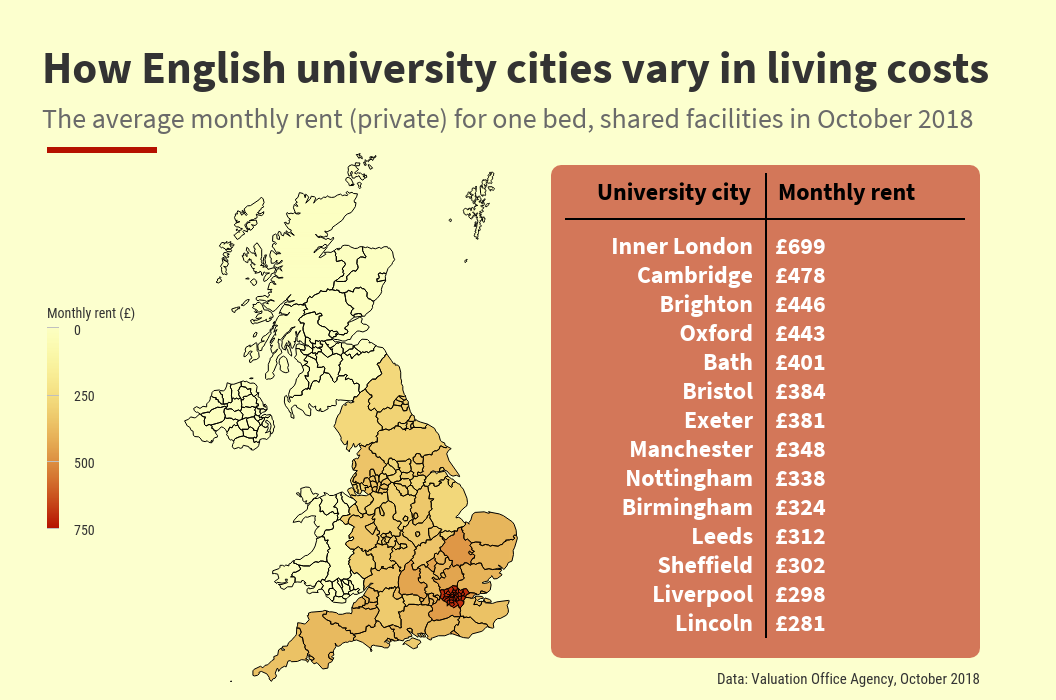

While tuition fees have no immediate financial impact on students, we eagerly await the latest text update from our SFE maintenance loan as much as our latest match on Tinder. The latest Valuation Office Agency (VOA) private renting survey for October 2018 shows an average monthly rent of £384 in Bristol for one room with shared facilities. However, the University of Bristol’s website lists an average of £435. Is the rising student population being exploited by the greater housing demands they create in a city?

Living costs are certainly a varying factor for students at universities across the UK. In the same VOA renting dataset, Bristol was the seventh most expensive major university city outside of London for a privately rented room in shared facilities behind Cambridge, Guildford, Bath, Reading, Bedford, and Ipswich. It is nearly 40 per cent more expensive to rent in Bristol as it is in Lincoln. Property price tends to be reflective of more general living costs as well.

Still, the maintenance loans are the same income based amounts for students in either Lincoln, Bristol, or Cambridge. It is only different in London, where the maximum maintenance loan is £11,002 compared to £8,430 outside the capital. The average rent in Bristol, £4,608 for the year, is 54 per cent of the maximum maintenance loan. Yet, as noted in the University’s average figures, most student actually pay more than that - student lettings are rarely below £400 per week and that does not include bills, agency fees and other hidden costs.

(Epigram / Patrick Sullivan)

The student loan system should encourage students from all background that finances should not dictate academic decisions. While the tuition fee loans are misperceived as the main driver putting off lower income students, the maintenance loan is what actually will affect all students in more expensive cities if they are not financially supported by their parents or universities.

Featured image: Unsplash / Philip Veater